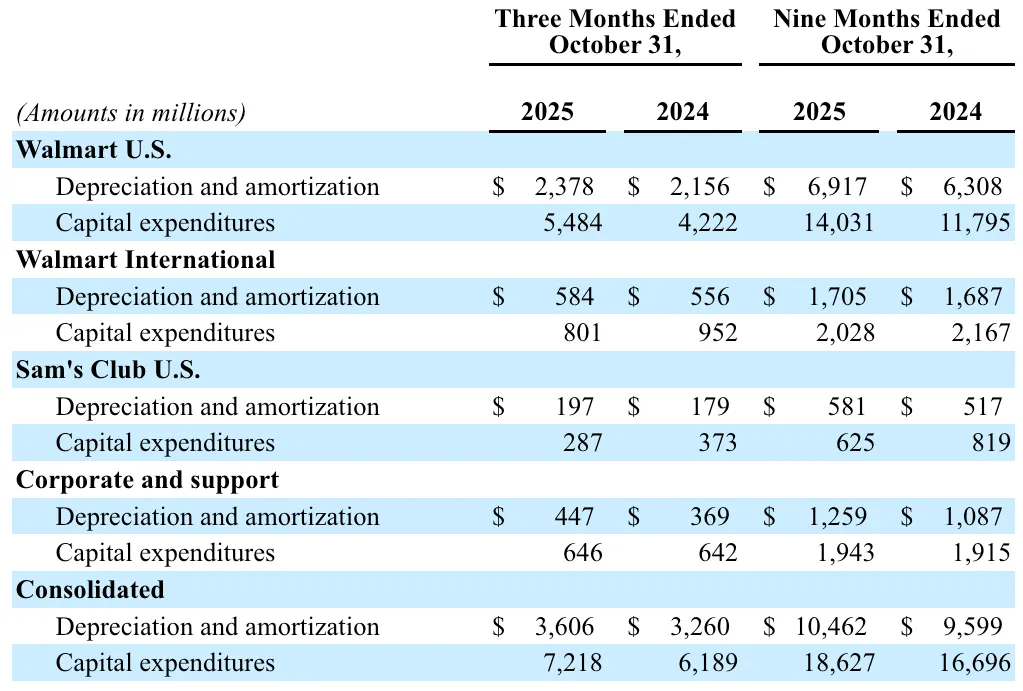

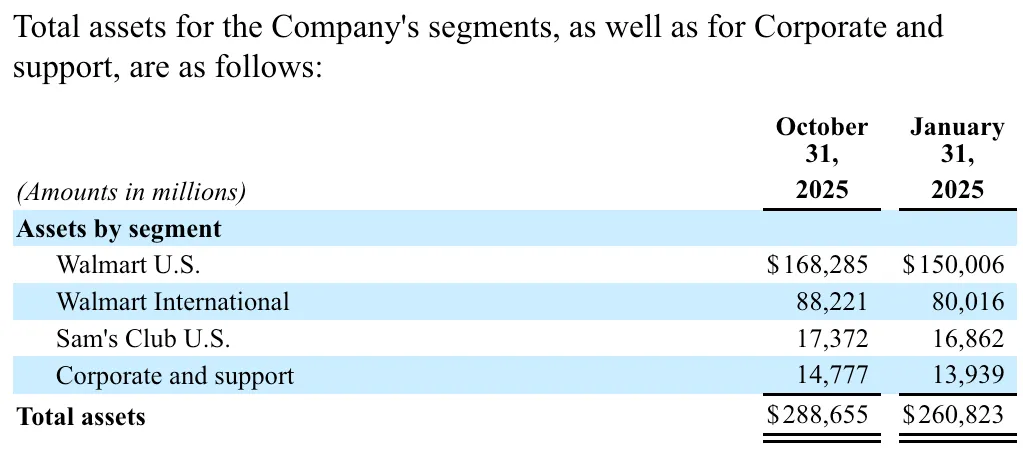

Depreciation and amortization and capital expenditures for the Company's segments, as well as for Corporate and support, are as follows:本公司各业务部门以及公司总部及支持部门的折旧、摊销和资本支出情况如下:Based on the financial data provided, here is an analysis of the key takeaways for investors, focusing on Walmart's growth strategy and capital allocation.根据所提供的财务数据,以下是从投资者角度对该公司增长战略与资本配置的核心要点分析。1. Massive Reinvestment in Walmart U.S.一、大幅加码美国本土业务再投资The most significant takeaway is the aggressive capital expenditure (CapEx) in the Walmart U.S. segment. For the nine months ended October 31, 2025, CapEx rose from $11.8 billion to over $14 billion year-over-year. This indicates that Walmart is doubling down on its domestic infrastructure—likely focusing on supply chain automation, store remodels, and e-commerce fulfillment—to maintain its competitive edge.最显著的动向是其美国本土业务板块的资本开支大幅增加。截至2025年10月31日的九个月内,资本支出同比从118亿美元增至逾140亿美元。这表明公司正全力强化本土基础设施建设,重点可能包括供应链自动化、门店升级改造及电商履约能力,以巩固其竞争优势。2. CapEx Outpacing Depreciation二、资本支出远超折旧摊销On a consolidated basis, Walmart’s CapEx ($18.6 billion) is significantly higher than its Depreciation and Amortization ($10.5 billion) for the nine-month period. For investors, this "growth CapEx" signals that the company is not just maintaining its current assets but is actively expanding its footprint and capabilities. This is a bullish indicator for long-term revenue capacity, though it places a short-term demand on cash flow.从合并报表看,该公司九个月的资本支出(186亿美元)显著高于折旧与摊销费用(105亿美元)。对投资者而言,这种“成长型资本支出”表明公司不仅在维护现有资产,更在积极拓展业务版图与运营能力。这是长期收入潜力的积极信号,尽管短期内对现金流构成压力。3. Divergent Strategies: International vs. Domestic三、国际与本土战略分化明显There is a clear trend of shifting resources. While the U.S. segments (Walmart U.S. and Sam's Club) show robust asset growth and high investment, Walmart International saw a slight decrease in nine-month CapEx (from $2.17 billion to $2.03 billion). This suggests a more disciplined or selective investment approach abroad compared to the high-growth "all-in" strategy seen domestically.资源倾斜趋势清晰可见:美国本土板块(含山姆会员店)资产增长强劲、投入力度大,而国际业务的九个月资本支出则略有下降(从21.7亿美元降至20.3亿美元)。这表明公司在海外采取更为审慎或选择性的投资策略,与本土“全力押注”的高增长路径形成鲜明对比。4. Significant Asset Growth四、总资产规模快速扩张The balance sheet has expanded rapidly in just nine months. Total assets grew from $260.8 billion in January to $288.7 billion in October. The fact that $18.2 billion of that $28 billion increase occurred within the Walmart U.S. segment reinforces that the domestic market remains the primary engine for the company’s valuation.资产负债表在短短九个月内迅速扩张:总资产从1月的2608亿美元增至10月的2887亿美元。其中,280亿美元增量中有182亿美元来自美国本土业务,进一步印证本土市场仍是公司价值增长的核心引擎。5. Rising Operating Costs (D&A)五、运营成本(折旧摊销)持续上升Investors should note the steady rise in Depreciation and Amortization (D&A) across all segments. As Walmart completes its massive capital projects, these costs will continue to rise, creating a "drag" on reported net income in future quarters. This makes EBITDA and Free Cash Flow more important metrics than simple Net Income when evaluating Walmart's performance during this heavy investment cycle.投资者需关注各业务板块折旧与摊销费用的稳步上升。随着大规模资本项目陆续完工,此类成本将持续增加,对未来季度的净利润形成“拖累”。因此,在当前重投资周期中,评估公司表现时,息税折旧摊销前利润(EBITDA)比单纯的净利润更具参考价值。6. Corporate and Support Efficiency六、总部与支持职能效率提升Despite the massive scale of the business, Corporate and support CapEx remained relatively flat for the nine-month period ($1.94 billion vs. $1.92 billion). This suggests that Walmart is successfully scaling its central operations efficiently without requiring a proportional increase in corporate overhead spending.尽管业务规模庞大,公司总部及支持性资本支出在九个月内基本持平(19.4亿美元 vs. 19.2亿美元)。这表明其在扩大整体运营的同时,有效控制了管理费用的增长,实现了高效集约化管理。Summary for Investors: Walmart is in a high-growth investment phase centered almost entirely on the U.S. market. While this creates higher depreciation expenses and uses significant cash, the massive increase in total assets suggests the company is aggressively positioning itself to dominate retail and logistics for the coming years.投资者摘要:该公司正处于以美国市场为核心的高增长投资阶段。尽管此举推高了折旧成本并消耗大量现金,但总资产的迅猛增长表明,公司正积极布局,力争在未来数年主导零售与物流领域。For more insightful content, long press the QR code to follow 更多深度好文长按关注