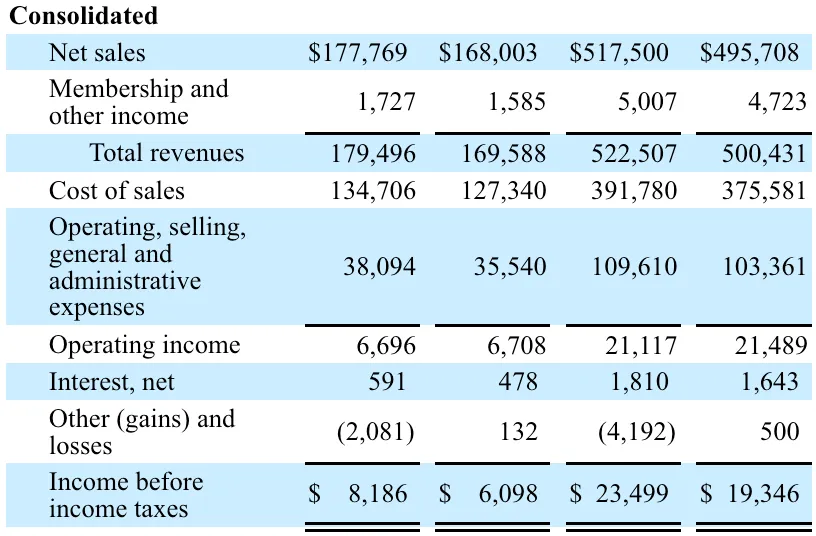

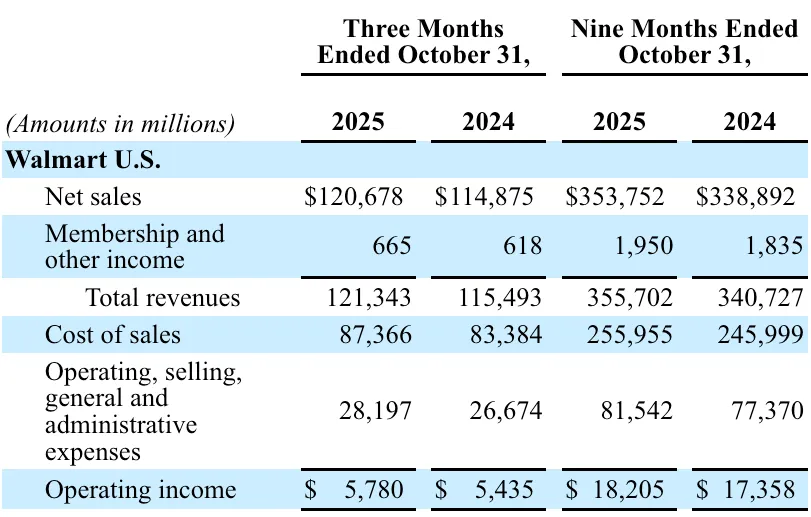

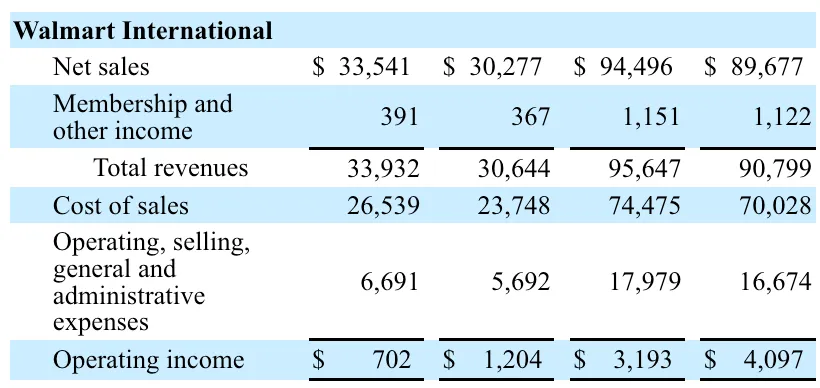

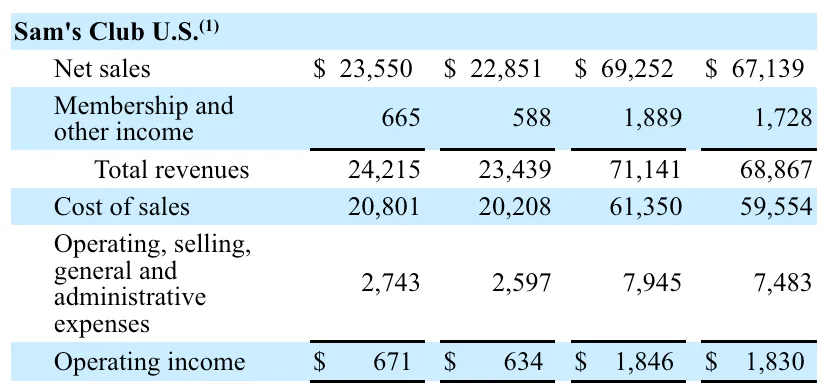

Based on the financial table provided, here is an analysis of how Walmart performed for the quarter (three months) and the year-to-date (nine months) ending October 31, 2025, compared to the previous year.根据所提供的财务数据,以下是对截至2025年10月31日的季度(三个月)及年初至今(九个月)业绩与上年同期的对比分析。1. The "Big Picture" (Consolidated Results)一、整体概况(合并结果)While Walmart’s total sales are growing, their actual profit from operations is slightly shrinking.尽管总销售额持续增长,但其实际经营利润却略有下滑。Total Revenue Growth: Up $9.9 billion (+5.8%) for the quarter.总收入增长:本季度增加99亿美元(+5.8%)。Operating Income Trend: Even though they sold more, their operating profit actually dropped by $12 million (-0.2%) for the quarter.经营利润趋势:尽管销量上升,本季度经营利润反而下降了1200万美元(-0.2%)。Why? The massive growth in the U.S. was offset by a very tough quarter for the International business and higher corporate costs.原因何在?美国本土业务的强劲增长,被国际业务的艰难表现及总部管理成本上升所抵消。2. Segment Breakdown (The "Winner" vs. The "Struggler")二、分部表现(“优等生”与“困难户”)Walmart U.S. (The Powerhouse)美国本土业务(核心引擎)This is the strongest part of the business. They managed to grow their profit faster than their sales, which usually means they are managing costs well or selling higher-margin items.这是公司最强势的板块。其利润增速超过收入增速,通常意味着成本控制得当或高毛利商品销售占比提升。Revenue: $121.3 Billion (Up 5.1%)收入:1213亿美元(同比增长5.1%)Operating Profit: $5.78 Billion (Up 6.3%)经营利润:57.8亿美元(同比增长6.3%)Operating Margin: 4.76% (Calculated as: )经营利润率:4.76%Walmart International (The Concern)国际业务(主要隐忧)This segment had a difficult quarter. While they brought in significantly more money (sales were up 10.7%), their profit crashed.该板块本季度表现艰难。尽管收入大幅增长(+10.7%),利润却急剧下滑。Operating Profit: Dropped from $1.2 Billion to $702 Million (a 41.7% decrease).经营利润:从120亿美元降至70.2亿美元(降幅达41.7%)。Operating Margin: Fell to 2.07% (compared to 3.93% last year).经营利润率:降至2.07%(上年为3.93%)。What this means: For every $100 in sales, International only kept about $2 in profit this year, whereas they kept almost $4 last year. This suggests their costs (like labor, shipping, or goods) rose much faster than their prices.这意味着:每100美元销售额中,国际业务今年仅留存约2美元利润,而去年接近4美元。表明其成本(如人力、物流或商品采购)涨幅远超售价提升。Sam’s Club U.S. (Steady & Reliable)山姆会员店美国业务(稳健可靠)Sam’s Club is showing very consistent, stable growth.山姆会员店展现出高度稳定、持续的增长态势。Operating Profit: Up 5.8% for the quarter.经营利润:本季度增长5.8%。Operating Margin: 2.77% (Calculated as: ). This is lower than Walmart U.S. because Sam's Club relies on high-volume, low-markup sales and membership fees.经营利润率:2.77%。低于美国本土超市,因其商业模式依赖高销量、低毛利商品及会员费收入。3.Summary Analysis三、综合研判If you were the "CODM" (the boss) mentioned in your previous question, your focus right now would be on Walmart International. You would be asking why profits dropped by nearly 42% even though sales were booming. You would likely be "allocating resources" to figure out if that segment has a spending problem or if international competition is forcing them to lower prices too much.若您是此前问题中提到的“首席运营决策者”,当前关注重点应放在国际业务上。您会追问:为何在销售额大幅增长的同时,利润却暴跌近42%?很可能会重新调配资源,排查该板块是否存在成本失控,或是否因海外市场竞争激烈而被迫过度降价。Meanwhile, you would be very happy with Walmart U.S., as it is providing the bulk of the company's cash flow ($18.2 billion in profit so far this year).与此同时,您会对美国本土业务感到非常满意——它正贡献公司绝大部分现金流(今年迄今已实现182亿美元利润)。For more insightful content, long press the QR code to follow 更多深度好文长按关注