J.P.Morgan

China Battery & Materials

Field trip sparks confidence: Confirm CATL as top pick, u/g Yunnan Energy (separator), d/g Hunan Yuneng (cathode)

• Stock recommendations: CATL – stay top pick. The company is notably less exposed to material price increases and is well-positioned for further market share gains. We maintain Neutral or UW ratings on tier-2 battery makers, as we see limited prospects for improved unit economics, which may result in these companies missing market expectations. Yunnan Energy (separator) – u/g to OW. We turned more positive on separator and expect the wet separator industry’s UTR to surpass its 2022 peak this year, with a 10ppt UTR improvement in 2026 and again in 2027E (see Figure 9). Hunan Yuneng (cathode) – d/g to Neutral. New capacity in this segment can be brought online quickly and easily, while battery manufacturers are increasingly incentivized to expand internal capacity through investments or strategic partnerships.

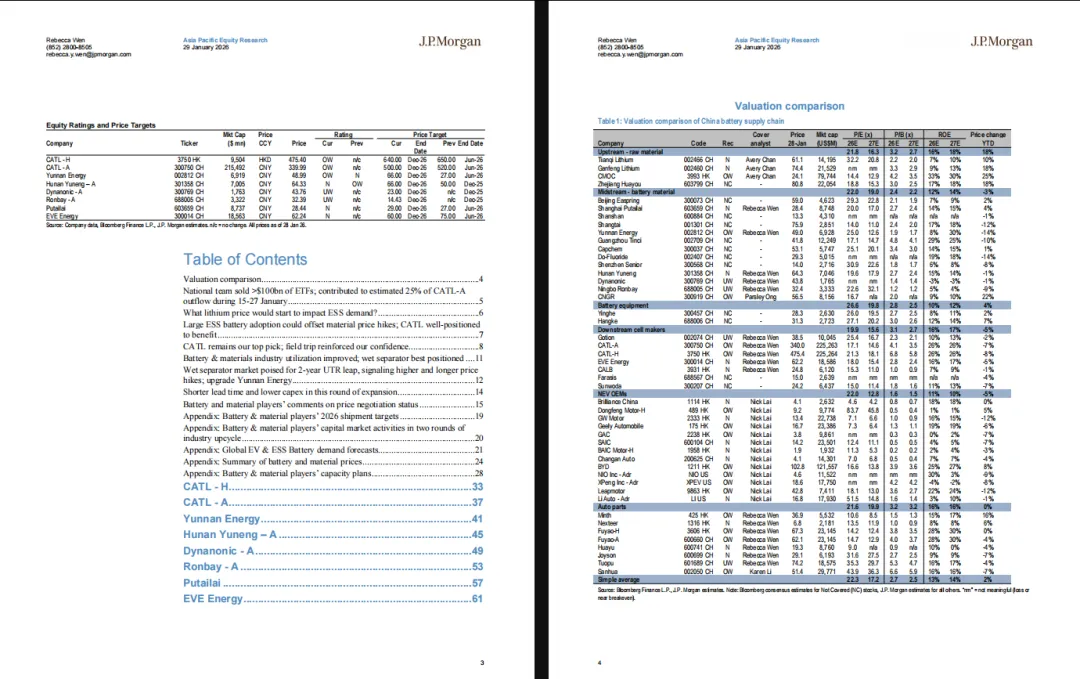

• An estimated 25% of CATL-A turnover sold by “national team”. CATL-A’s share price has fallen 7% YTD, underperforming CSI300 by 9% and CSI1000 by 18%. We believe this may be due to China Central Huijin Investment selling ETFs, as Bloomberg has reported, and CATL being heavily-weighted in CSI300. We estimate the national team contributed to 25% of CATL-A’s turnover during January 15-27 (24% during Jan 15-22, accelerating to 28% during Jan 23-27). Bloomberg Intelligence estimates a maximum further $90bn sales by the national team before LNY.

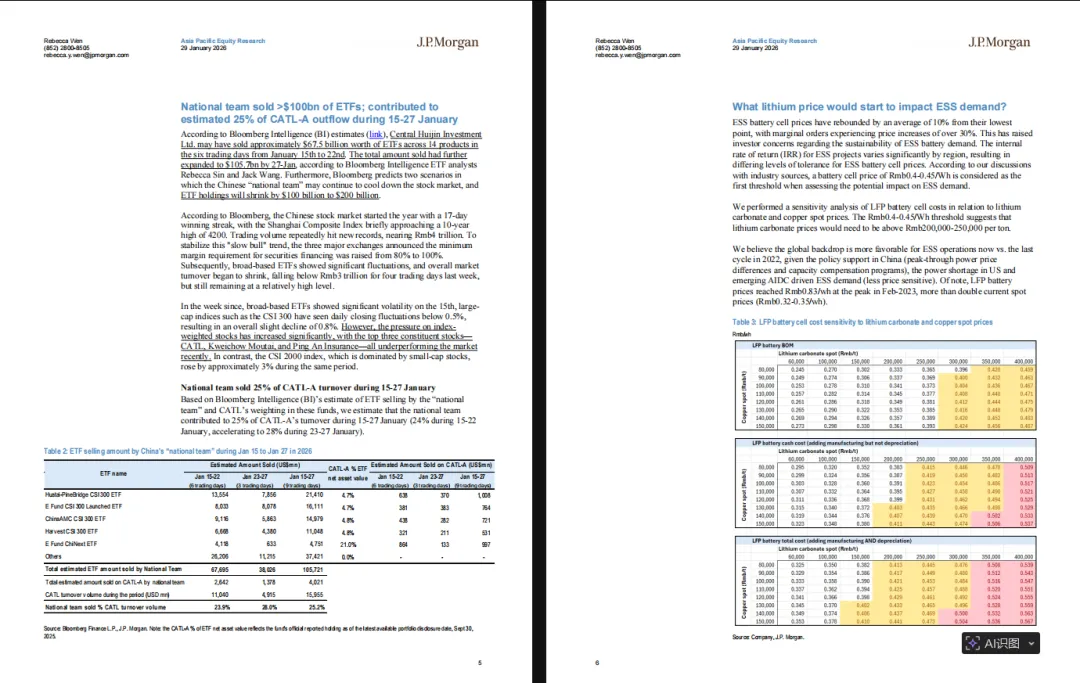

• Industry demand remains robust, with ESS battery makers—including tier-3 players—operating at full capacity and production lines booked through midyear. This strong outlook has persisted since late-2025, with only minor volatility linked to export tax rebate changes, and no typical slowdown during Lunar New Year. At what lithium price might demand begin to soften?

While IRR sensitivity varies by region, some industry participants estimate that demand could be affected when battery cell prices reach Rmb0.40–0.45/wh, which corresponds to lithium carbonate spot at Rmb200k-250k/t (Table 3). Notably, current IRR conditions are more favorable than in previous cycles, and battery prices are now less than half of their 2022 peak.

• Can battery makers pass through the material cost inflations? Most battery makers now embed lithium carbonate prices in contract formulas, enabling smooth cost pass-through, while non-lithium cost increases are negotiated with mixed success. Overseas ESS customers are generally more receptive to price adjustments while talks with domestic EV OEMs or large domestic ESS

... ...

请扫码加入知识星球【行业报告汇】自行下载。

会员期(1年)内星球所有更新的报告均可自由下载。