说明 Note:

仅用于中英文写作训练,无其他目的。

For Chinese‑English writing practice only, with no other intent.

我对茅台的财报从2000年到2025年进行了历史性跟踪,试图寻找影响其商业变化的本质因素。但由于缺少相关的一手信息和数据,目前尚未得出明确结论。我排除了“消费者消费变化”和“政策”因素,这两者更多属于表象,而非本质因素。

I have tracked Moutai’s financial reports from 2000 to 2025, attempting to identify the fundamental factors driving its business changes. However, due to a lack of primary information and data, no definitive conclusion has been reached. I have ruled out “changes in consumer spending” and “policy” as factors, as these are more superficial than fundamental.

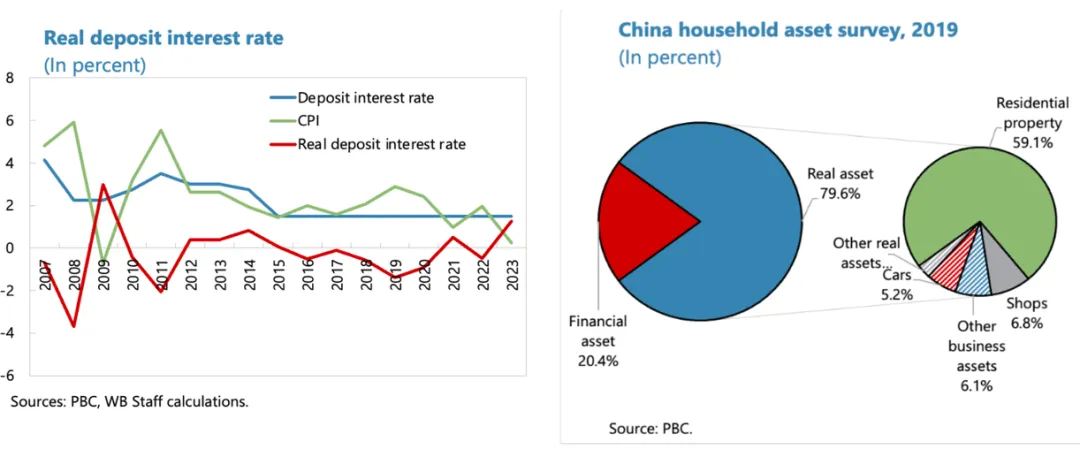

分析显示,茅台乃至整个白酒行业的情况,与结构性的宏观经济有直接联系。由于这一阶段出现重大突发事件,例如新冠疫情以及随后的房地产危机,这些都直接或间接影响了中国家庭资产结构与消费预期。简而言之,房地产占家庭资产的高比重是中国的一个显著特点,而房地产市场的波动会显著影响家庭财富感知。

The analysis shows that Moutai’s situation—and that of the overall baijiu industry—is directly linked to structural macroeconomic forces. During this period, major shocks such as the COVID‑19 pandemic and the subsequent real estate crisis have directly or indirectly affected Chinese household asset structures and consumption expectations. In short, the high share of real estate in household wealth is a prominent characteristic of China, and fluctuations in the housing market significantly affect perceived household wealth.

中国家庭资产中房产占据了较大比例,而在英美等发达国家,金融资产占比明显更高。根据相关调查,中国家庭非金融资产(主要是房产)占家庭总资产的比重长期保持在较高水平,这意味着房价变动对家庭财富影响更直接。

From the chart below, we can see that property constitutes a large proportion of Chinese household assets, whereas in developed countries such as the United States and the United Kingdom, financial assets make up a higher share. According to wealth surveys, non‑financial assets (primarily real estate) have historically accounted for a high share of Chinese household total assets, meaning that housing price movements have a more direct impact on household wealth.

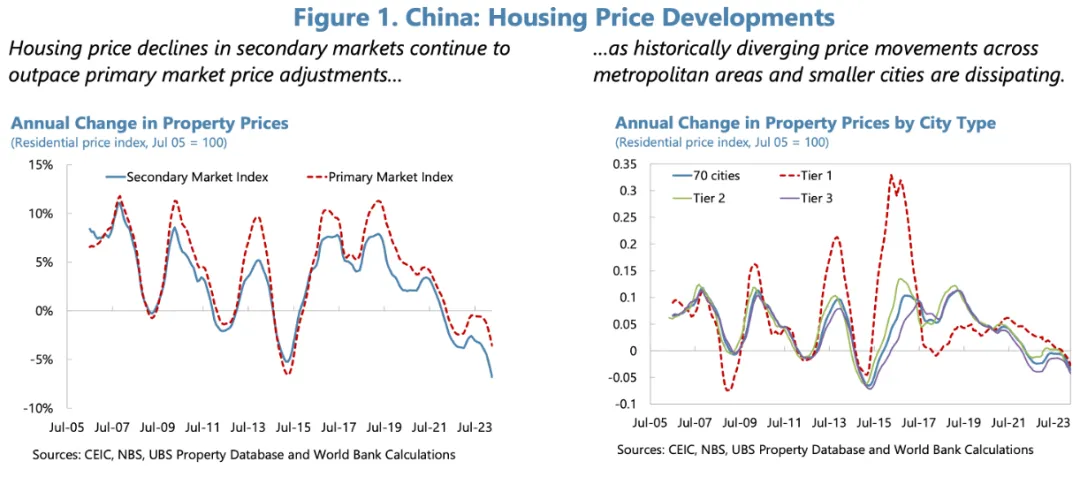

下图显示了中国房价的长期变化趋势。可以看到,自近年来房地产市场进入调整周期后,房产价值整体承压。这会直接影响个人财务状况:对于拥有房产或依赖租金收入的家庭来说,他们会明显感受到“账面财富缩水”。

The next chart shows the long‑term trend in Chinese housing prices. It is evident that since the real estate market entered an adjustment cycle in recent years, property values have been under pressure. This directly affects personal finances: for households owning property or relying on rental income, there is a clear sense of “paper wealth erosion.”

从消费者心理层面看,这可以解释为何在经济下行压力下,人们会减少对非必需品或高价商品的支出。这种消费预期的改变或许是茅台这几年业绩不佳的部分原因之一。

From the consumer psychology perspective, this helps explain why under economic pressure people reduce spending on non‑essential or high‑priced items. This change in consumption expectations may be one of the reasons behind Moutai’s weaker performance in recent years.

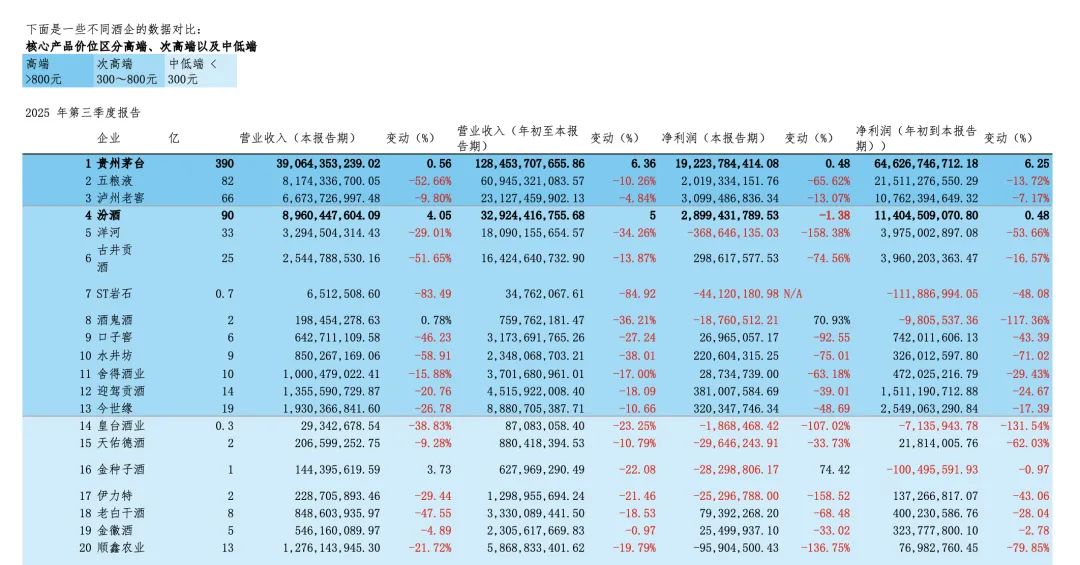

但仍需解释一个现象:为何部分白酒企业的低端产品表现比高端产品更疲弱。一个较简单的理解是,当经济压力较大时,低收入群体更易感受到压力,并倾向于削减所有可选支出,从而对低端产品的需求也大幅下降。

However, one question remains: why have some low‑end products underperformed even more than high‑end ones? A straightforward interpretation is that when economic pressure is significant, low‑income households feel it most acutely and tend to cut all discretionary spending, leading to a sharp reduction in demand for low‑end goods as well.

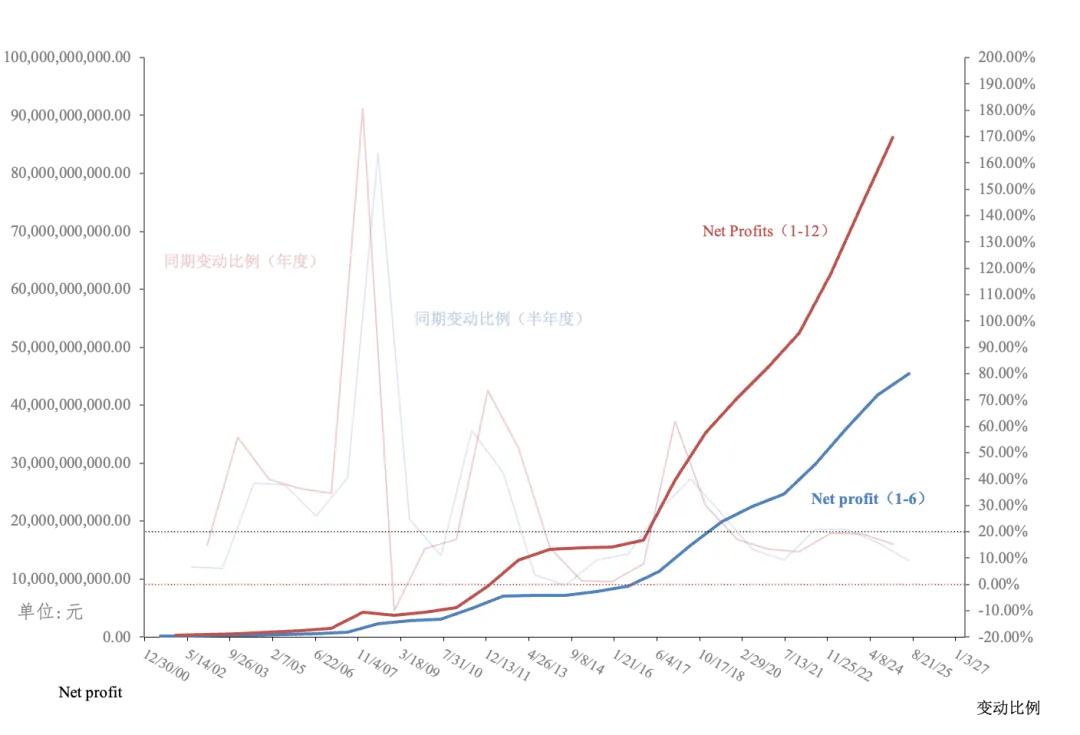

从下图我们可以看到,茅台近几年的表现不容乐观,整个行业也呈现出一片萧条之势,尤其是从去年(2025年)各个行业第三季度的财报结果来看。分析其他酒企可能不会得到太多有意义的结论,因此我主要专注于分析茅台,目的是尝试找出影响整个白酒行业的本质原因。我之前提到过,我的分析认为茅台目前的状况并不是由于企业自身的问题或行业内部出现了根本性变化,而是由经济结构造成的一种大趋势。这种趋势可能为未来的发展留下难以避免的阴霾,这是我最担心的部分。如果问题不在于公司和行业本身,那么问题就可能出在整个宏观经济环境。这意味着2026年可能比2025年更加艰难,尤其对于即将毕业的学生、正在实习或依靠短期合同工作的毕业生来说将更为不易;对于传统行业和金融行业而言,这一年也可能更加困难。

From the chart below, we can see that Moutai’s performance in recent years has been far from encouraging, and the entire industry appears to be under significant strain, especially judging by the third‑quarter financial results across sectors last year (2025). Analyzing other liquor companies may not yield many meaningful insights, so I have focused my analysis on Moutai with the aim of uncovering the fundamental reasons affecting the entire baijiu industry. As mentioned earlier, my analysis suggests that Moutai’s current situation is not primarily due to internal corporate issues or a fundamental breakdown within the industry itself, but rather driven by broader economic structural forces. This trend may cast a foreseeable shadow over future development, which is my greatest concern. If the problem does not lie with the company or the industry, then it likely stems from the macroeconomic environment as a whole. This implies that 2026 may be even more challenging than 2025, particularly for graduating students, those in internships or on short‑term contracts, and recent graduates navigating uncertain job paths. It may also be a particularly difficult year for traditional and financial industries.

此外,我初步判断此次房地产市场调整可能长期影响中国家庭资产结构,人们可能会加速将资产配置向金融资产等其他类别倾斜,以寻求更高的流动性和风险分散。

Additionally, my initial assessment is that this real estate market adjustment may have a lasting impact on Chinese household asset structures, potentially accelerating a shift toward financial assets for greater liquidity and diversification.

待更新……

To be updated…