拆解携程 2026Q1 财报藏着的酒店转型信号

2026-06-25 21:11

拆解携程 2026Q1 财报藏着的酒店转型信号

The Warning Behind 16.2 Billion RMB2026年Q1,携程交出了一份让财经媒体"兴奋"的数据:The numbers look impressive. But hotel managers need to look deeper.- 住宿业务 2023 年复苏阶段单季最高增速达 131%(2023Q4),2023Q3 增速 92%,如今回落至 2026Q1 的 17%。

- Q2营收指引仅增3%-8%,剔除疫情因素,创携程上市以来单季最低增速

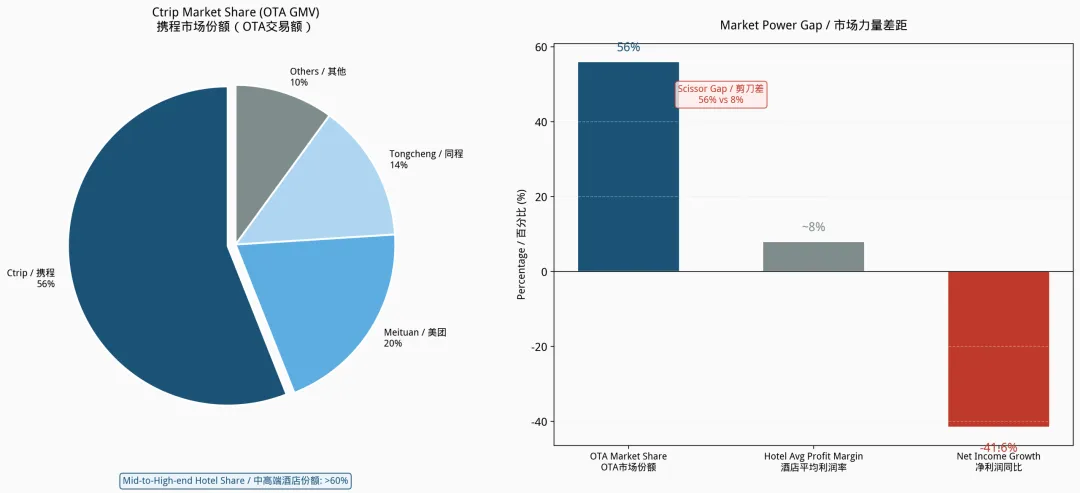

更值得警惕的是:携程在财报中明确披露——"可能对综合财务状况产生重大不利影响"。This article dissects what these numbers mean for hotel operators, not investors.Chapter 1: Decoding 6.5B Accommodation Revenue - Three TruthsTruth 1: Accommodation Growth First Time Below Group AverageThe accommodation booking business is shifting from "growth engine" to "stable base."这不是携程的问题,而是整个国内在线旅游流量红利见顶的信号。This is not Ctrip's problem alone—it's a signal that online travel traffic dividends are exhausted.真相二:住宿毛利率>80%,酒店利润率<10%的结构性矛盾Truth 2: Structural Contradiction - OTA Margin >80% vs Hotel Margin <10%- 大部分成本是服务器和人工,无需承担客房租金、折旧、人力

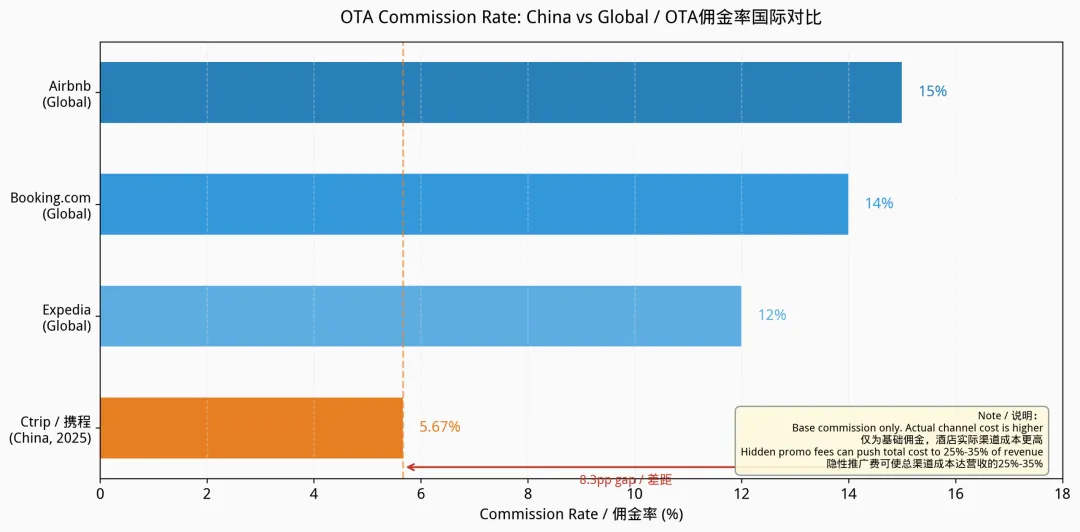

问题核心:作为流量平台的携程,拿走了住宿价值链中不成比例的利润。The core issue: as a traffic platform, Ctrip captures disproportionate profits from the accommodation value chain.Truth 3: Hidden Costs Behind 5.67% Commission Rate- 隐性推广费:部分酒店营销投入可达营收的15%-20%

- 综合渠道成本:部分高星酒店反映实际支出占营收的25%-35%

导致大量住宿企业在2025年12月发起反垄断维权。.第二章:Q2指引的断崖——从17%到3%-8%意味着什么Chapter 2: Q2 Guidance Cliff - What 3%-8% Growth MeansLowest Single-Quarter Growth Since IPO (Excluding COVID)回顾携程历史数据,即使在疫情最严重的2020年Q2,由于基数效应,携程仍实现了环比增长。而这一次,是真真切切的增速断崖。This is a genuine growth cliff, not a statistical artifact.High energy prices are compressing consumer travel budgets globally. European and Middle Eastern tourism markets are experiencing cost pressures that trickle down to Chinese outbound and domestic travel.Geopolitical tensions are creating uncertainty. Business travel and high-end leisure travel are particularly sensitive to travel advisories and visa complications.Compliance adjustments are the real driver. In the Q1 earnings call, Ctrip management explicitly stated: "针对行业标准和合规框架的最新变化,主动进行了相应的运营调整"Chapter 3: Antitrust Storm - The Biggest Variable for HotelsRegulatory Timeline H1 2026- 6月11日:市监总局/网信办/国家铁路局联合约谈7家OTA

- 6月13日:上海网信办罚款1000万元(数据出境违规)

Six regulatory actions in six months. This is unprecedented.What "Exclusive Dealing" Relaxation Means- Hoteliers can list on multiple OTAs without exclusivity penalties

- Better price discovery across platforms

- Reduced dependency risk on single channel

- Channel management costs will increase

- Price parity maintenance becomes more complex

- Need better inventory management systems

Real Impact of "Price Adjustment Assistant" Shutdown2026 年 3 月,在多地监管约谈整治算法无序定价的背景下,携程主动下线 “调价助手”;有酒店经营者反馈,该工具全年自动调价超 30 次,直接压缩门店 40% 利润。Potential Fines: 1.9-3.1 Billion RMB仅投行机构测算,最终处罚金额以市监总局官方公告为准,不构成法律 / 投资预判”

Chapter 4: Inbound Tourism - Structural Growth for HotelsQ1 Data: 7M Tourists, 5.1 Days Average Stay高星酒店是入境游的首选。这意味着每接待一位欧美入境游客,酒店获得的不仅是更高的客单价,还有更长的停留时间和更高的复购潜力。New Opportunities in Tier-3/4 Cities一个容易被忽视的数据:入境游增量超过一半来自三线及以下城市。洛阳、大同、开封、景德镇等城市承接的入境游订单酒店总量两年增幅超过200%。二三线城市的高星酒店,现在有了新的客源——不是来自国内商务客,而是来自海外休闲游客。Ctrip's 5-Year Strategic Target- 开通国际信用卡/VISA/MasterCard支付

Chapter 5: Consumer Trends - Three High-Value SegmentsSmall Group Tours: 55% Higher Per Capita SpendingEvent Tourism: 74% Booking Increase演唱会、体育赛事、戏剧展演带动的旅游预订同比+74%。这意味着:Silver Tourists: 10% of Users, 30% Higher Purchasing Power银发旅客(60岁以上)占携程平台用户10%,但购买力高30%。这个群体的特点:相关数据显示OTA平台营收增速显著高于国内外连锁酒店,价值链利润向上游平台集中。Chapter 6: Operational Decision Guide - Six RecommendationsChannel Strategy: Seize Antitrust Window, Rebuild Direct Booking

Inbound Tourism: Systematically Improve Reception Capacity- 支付:VISA/MasterCard/AMEX/JCB全通道

- 公关:海外点评平台(TripAdvisor,Booking.com, Agoda,Yelp, etc.)管理

Product Strategy: Customize for Small Groups/Events/Silver Tourists建议四:定价策略——摆脱OTA价格锚定,恢复自主定价Pricing Strategy: Break Free from OTA Price Anchoring- 设立价格最低保证(Best Rate Guarantee)

Commission Negotiation: Best Time to Renegotiate监管压力下,OTA对大型连锁/高星酒店的态度正在软化。

Data Asset: Reduce Dependency on OTA Data

Conclusion: As Ctrip Changes, Hotels Must Change Too中立角度作者认为携程为中小酒店、三四线文旅城市带来海外入境客源,是酒店全球化分销重要渠道;调价助手工具初衷是辅助收益管理,异化源于无约束自动跟价机制,而非工具本身完全无价值;平台投入大量海外营销、服务器、客服成本,高佣金背后对应全域流量供给,矛盾核心是定价权不对等、隐性推广强制消费,而非佣金本身。携程Q1财报,表面是162亿的营收增长,背后是三重结构性变化:

作为酒店管理者,我们不能只看携程的股价走势,更要看清这些数字背后的产业逻辑。This article is for hotel industry managers. Views expressed are the author's own. All data sourced from public disclosures.