台积电Q1前瞻TSMC Q1 Earnings Preview Report核心观点 / Key Highlights台积电的Q1财报电话会议定于4月16日收盘后举行。我们预计业绩将达到Q1指引的高端,美元销售额环比增长6%,毛利率达64.8%。我们认为管理层可能会重申2026年指引,即美元销售额增长30%,资本支出520-560亿美元。云计算AI需求持续加强,但我们认为供应限制将限制台积电今年实现显著上行的空间。TSMC's Q126 earnings call is scheduled for after market close on 16 April. We anticipate results to reach the higher end of Q1 guidance, with sales up 6% QoQ in USD and GM at 64.8%. We think management is likely to reaffirm 2026 guidance for 30% sales growth in USD and US$52-56bn capex. Cloud AI demand continues to strengthen, but we think supply constraints will limit meaningful upside for TSMC this year.然而,由于内存短缺和内存成本通胀,消费需求正在走弱,可能会限制下半年增长,但如果对台积电有任何影响,应该也是微乎其微的。中东紧张局势增加了宏观不确定性,但考虑到AI对超大规模厂商和企业的重要性,AI支出应能保持隔离,除非冲突旷日持久。Consumer demand, however, is weakening as a result of memory shortage and memory cost inflation, and may cap growth into H226, although the impact on TSMC, if any, should be minimal. Middle East tensions add a layer of macro uncertainty, but AI spend should stay insulated, barring a protracted conflict, given its strategic importance to hyperscalers and corporates.Q2展望 / Q2 Outlook在Q1表现好于季节性之后,我们预测Q2销售额环比增长7%,毛利率稳定在64.8%。目前可见度表明,2026年台积电的N4、N3和N2产能将全面满载。Following a better-than-seasonal Q1, we forecast Q2 sales to grow 7% QoQ with GM stable at 64.8%. Current visibility suggests full utilization across N4, N3 and N2 at TSMC through 2026.大多数新的云计算AI加速器今年正在从N4升级到N3,到今年年底可能贡献台积电N3需求的约60%,而2026年初这一比例不到10%。我们上调了对台积电资本支出的预测,2027年预测为650亿美元,2028年预测为750亿美元(之前2026年预测为560亿美元),这得益于台积电加速N3和N2产能扩张。Most new Cloud AI accelerators are upgrading to N3 from N4 this year, and could contribute ~60% of TSMC's N3 demand by the end of this year, up from <10% in early 2026. We raised our estimates of TSMC's capex to US$65bn in 2027E and US$75bn in 2028E (from US$56bn in 2026E), underpinned by TSMC's accelerating N3 and N2 capacity expansion.我们认为N2的产能提升速度应快于N3量产前三年的速度。我们预测N2装机容量到2026年底达到90kwpm(之前为80kwpm),到2027年底达到140kwpm。We think the N2 ramp should be faster than N3 in its first three years of mass production. We forecast N2 installed capacity to reach 90kwpm (previously 80kwpm) by end-2026 and 140kwpm by end-2027.财报电话会议焦点 / Earnings Call Focus1) 中东冲突:我们认为氦气供应紧张对台积电生产的影响有限。根据我们的分析,电力成本每上涨10%可能会使台积电的毛利率降低0.2-0.3%。1) Middle East conflict: we see limited disruption from tight helium supply on TSMC's production. Every 10% rise in electricity cost could lower TSMC's GM by 0.2-0.3% based on our analysis.2) 整体半导体周期展望,以及智能手机/PC需求疲软可能带来的阻力(如有):瑞银对云计算AI计算需求持乐观态度,预计2026/27年半导体(不含内存)收入将增长25%/17%。瑞银最近将2026年智能手机单位出货量预测下调至下降10%。2) Overall semi cycle outlook, and headwinds, if any, from softening smartphone / PC demand: UBS is positive about Cloud AI compute demand and forecasts semis (ex memory) revenue to grow 25%/17% in 2026/27. UBS recently lowered smartphone unit sell-in to a 10% decline in 2026E.3) AI加速器增长对比2024-29年复合年增长率50%中高位的指引。3) AI accelerator growth vs guidance of mid to high 50% CAGR in 2024-29.4) 台积电解决供应紧张和管理来自英特尔和三星代工厂竞争的资本支出策略。4) TSMC's capex strategy to resolve tight supply and manage competition from Intel and Samsung Foundry.估值 / Valuation我们维持买入评级和2500新台币的目标价。我们的目标价基于21倍2027年预期市盈率,长期盈利复合年增长率为21%。我们预计台积电在2026年将跑赢更广泛的科技供应链,考虑到前沿需求的强劲前景、技术领先地位提升综合定价,以及在旷日持久的冲突中应能保持防御性的合理估值。We reiterate Buy and price target of NT$2,500. Our PT is based on 21x 2027E PE with a 21% long-term earnings CAGR. We anticipate TSMC will outperform the broader tech supply chain in 2026, given the robust outlook for leading-edge demand, strong technology leadership lifting blended pricing, and a reasonable valuation which should keep it defensive amidst a prolonged conflict.关键财务数据 / Key Financial Data

项目

Item

12个月评级

12-month rating

买入

Buy

12个月目标价

12-month price target

新台币2,500元

NT$2,500.00

当前股价(2026年3月27日)

Price (27 Mar 2026)

新台币1,840元

NT$1,840

交易数据

Trading Data

52周范围

52-wk range

新台币2,015-785元

NT$2,015-785.00

市值

Market cap.

新台币47,719十亿/美元1,493十亿

NT$47,719b/US$1,493b

流通股数

Shares o/s

25,934百万股

25,934m (ORD)

自由流通量

Free float

87%

87%

日均成交量(千股)

Avg. daily volume ('000)

41,682

41,682

日均成交额(百万)

Avg. daily value (m)

新台币75,374

NT$75,374

每股盈利(瑞银,摊薄)单位:新台币

EPS (UBS, diluted) (NT$)

2025年预期

12/25E

66.26

66.25

2026年预期

12/26E

90.58

89.85

2027年预期

12/27E

118.77

111.83

台积电平台驱动因素摘要 / TSMC Platform Driver Summary

台积电增长驱动因素

TSMC Growth Drivers

2015

2020

2025

2026E

2027E

15-20复合增长率

20-27E复合增长率

高性能计算-台积电

HPC - TSMC

$5.9B

$14.9B

$70.3B

$102.7B

$141.6B

21%

38%

高性能计算-市场

HPC - Market

$34.4B

$48.8B

$93.9B

$132.0B

$178.5B

7%

20%

台积电增长率

TSMC growth (%)

17%

30%

74%

77%

78%

20%

汽车-台积电

Automotive - TSMC

$1.1B

$1.5B

$6.1B

$6.7B

$7.7B

8%

移动设备-台积电

Mobile - TSMC

$11.6B

$21.9B

$35.8B

$37.7B

$43.2B

14%

物联网-台积电

IoT - TSMC

$1.1B

$3.7B

$6.1B

$6.4B

$7.4B

10%

来自主要客户的收入(单位:百万美元) / Revenue from Top Customers (US$m)

客户

2024

2025

2026E

2027E

占比

苹果

Apple

$19,393

$23,194

$29,704

$35,505

25.3%

英伟达

NVIDIA

$10,865

$22,268

$32,482

$43,993

20.4%

AMD

AMD

$8,336

$11,520

$15,196

$22,944

11.1%

博通

Broadcom

$4,024

$5,281

$13,953

$23,838

11.6%

英特尔

Intel

$7,615

$9,489

$8,486

$7,831

5.3%

高通

Qualcomm

$7,910

$9,448

$9,481

$10,576

6.0%

联发科

MediaTek

$4,370

$5,278

$5,708

$8,521

4.1%

美满电子

Marvell

$1,505

$2,333

$3,184

$4,364

2.0%

N3供需分析 / N3 Supply and Demand Analysis

客户/产品

N3产能需求(千片/月)

Q126E

Q226E

Q326E

Q426E

全年需求(千片)

英伟达

Nvidia

Rubin

Rubin

0

7

15

23

132

Rubin CPX

Rubin CPX

0

0

1

5

18

Vera CPU

Vera CPU

0

1

2

6

28

博通/谷歌/Meta/OpenAI

Broadcom/Google/Meta/OpenAI

谷歌TPU v7/v8AX

Google TPU v7/v8AX

6

11

16

21

161

AMD MI355

AMD MI355

2

2

1

1

18

亚马逊Trainium 3

Amazon Trainium 3

0

2

5

10

51

云计算AI合计需求

Capacity requirement - Cloud AI (kwpm)

9

25

51

99

553

云计算AI占N3需求比例

% of N3 demand

7%

20%

35%

58%

32%

苹果

Apple

iPhone应用处理器

iPhone's apps processor

38

35

31

24

385

Mac处理器

Mac's processor

10

10

10

6

106

iPad Pro & Air的M处理器

iPad's M processor

14

11

12

9

135

高通旗舰手机SoC

Qualcomm flagship smartphone SoC

17

13

9

4

129

联发科旗舰手机SoC

MediaTek flagship smartphone SoC

5

3

3

2

39

消费电子和其他设备合计

Capacity - Consumer and other devices (kwpm)

110

103

96

73

1,149

消费电子占N3需求比例

% of N3 demand

93%

80%

65%

42%

68%

N3总需求

Total N3 demand

119

128

147

172

1,701

台积电N3产能

TSMC's N3 capacity

120

130

150

170

1,710

产能利用率

Capacity utilisation

99%

99%

98%

101%

99%

运营指标 / Operating Metrics

指标

Q125

Q225

Q325

Q425

Q126E

Q226E

Q326E

Q426E

2025

2026E

产能(万片/年,8寸等效)

Capacity (WPO/Y, kpcs 8° eq.)

9,719

10,022

10,326

10,461

10,563

10,731

10,731

10,866

40,528

42,890

出货量(万片/年,8寸等效)

Shipment (WPO/Y, kpcs 8° eq.)

7,333

8,366

9,191

8,912

8,797

8,811

9,619

9,603

33,802

36,831

产能利用率

Utilization rate (%)

75%

83%

89%

85%

83%

82%

90%

88%

83%

86%

平均售价(美元)

ASP (US$)

2,962

3,062

3,132

3,246

3,420

3,654

3,715

3,833

3,108

3,660

总收入(新台币百万)

Total Revenue (NT$m)

839,254

933,792

989,918

1,046,090

1,112,347

1,190,211

1,332,426

1,372,399

3,809,054

5,007,382

资本支出(百万美元)

Capex (US$m)

10,058

9,567

9,608

11,493

14,000

14,000

14,000

14,000

40,739

56,000

毛利率

Gross margin (%)

58.8%

58.6%

59.5%

62.3%

64.8%

64.8%

63.5%

63.1%

59.9%

64.0%

营业利润率

Operating margin (%)

48.5%

49.6%

50.6%

54.0%

55.4%

56.0%

54.8%

54.1%

50.8%

55.0%

瑞银盈利预测 / UBS Earnings Forecasts

新台币百万

(NT$ mn)

2024

Q125

Q225

Q325

Q425

2025

Q126E

Q226E

Q326E

Q426E

2026E

收入

Revenue

2,894,308

839,254

933,792

989,918

1,046,090

3,809,054

1,112,347

1,190,211

1,332,426

1,372,399

5,007,382

同比变化

- YoY chg (%)

34%

42%

39%

30%

20%

32%

33%

27%

35%

31%

31%

环比变化

- QoQ chg (%)

-

-3%

11%

6%

6%

-

6%

7%

12%

3%

-

美元收入(百万)

Revenue (US$ mn)

90,184

25,526

30,070

33,097

33,731

122,031

35,201

37,665

42,165

43,430

158,461

毛利润

Gross profit

1,624,354

493,395

547,369

588,543

651,987

2,281,294

720,317

771,067

845,816

865,782

3,202,982

毛利率

- Gross margin

56.1%

58.8%

58.6%

59.5%

62.3%

59.9%

64.8%

64.8%

63.5%

63.1%

64.0%

营业利润

Operating profit

1,322,053

407,081

463,424

500,685

564,903

1,936,092

615,834

666,170

730,769

742,238

2,755,011

营业利润率

- OP margin

45.7%

48.5%

49.6%

50.6%

54.0%

50.8%

55.4%

56.0%

54.8%

54.1%

55.0%

税前利润

Pre-tax profit

1,405,839

430,895

493,035

525,369

592,363

2,041,663

634,781

684,447

749,768

762,701

2,831,697

净利润

Net profit

1,173,268

361,564

398,273

452,301

505,744

1,717,883

530,370

554,730

626,384

637,184

2,348,668

报告每股收益(新台币)

Reported EPS (NT$)

45.25

13.95

15.36

17.44

19.50

66.26

20.45

21.39

24.16

24.57

90.58

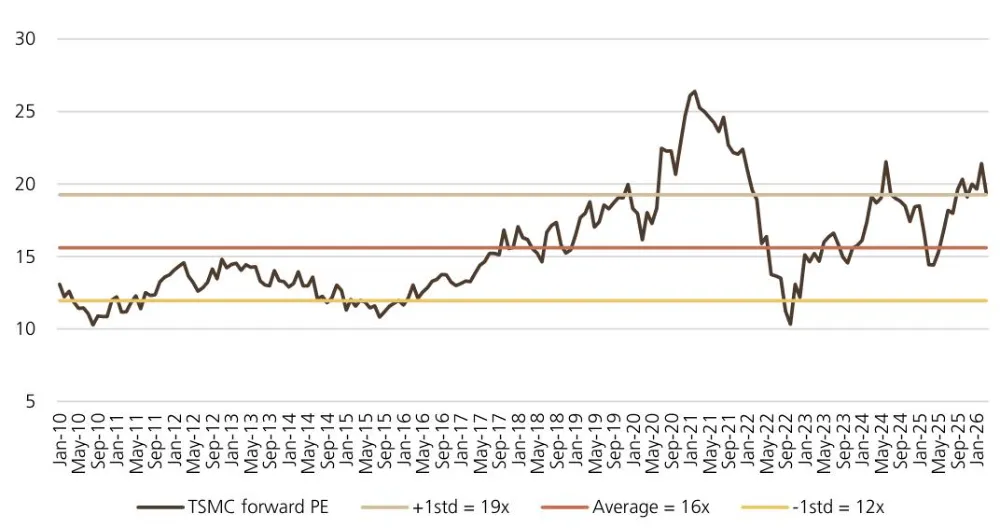

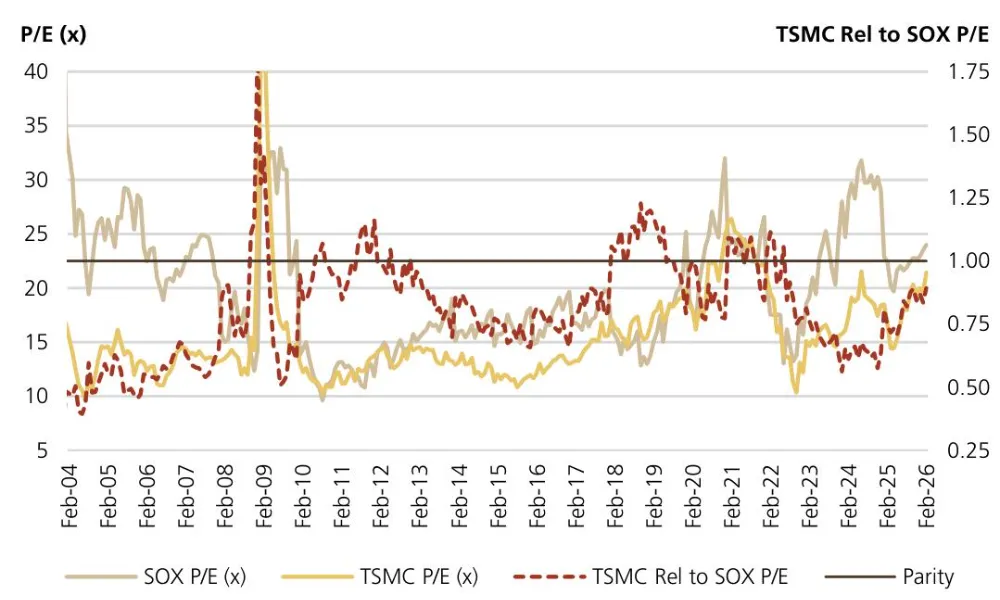

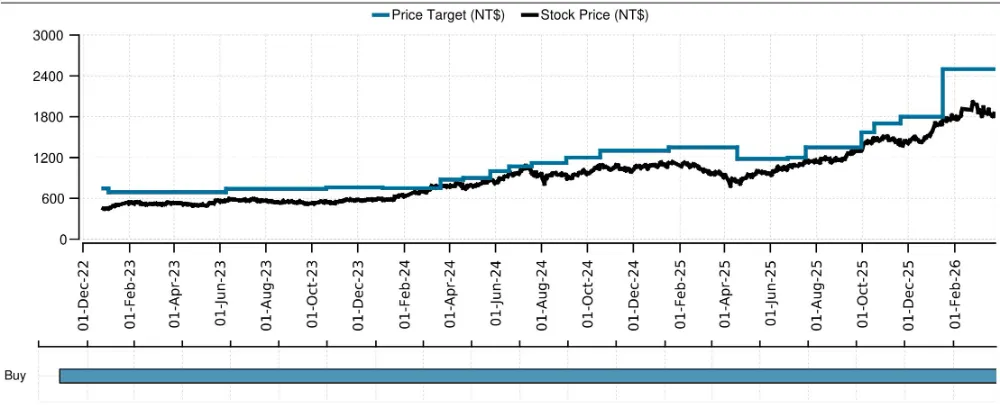

估值图表 / Valuation Charts图7:台积电12个月前瞻市盈率bandFigure 7: TSMC's 12-month forward PE band图8:台积电相对SOX估值仍有折让Figure 8: TSMC's valuation still at a discount to SOX图9:台积电股价走势图Figure 9: Taiwan Semiconductor Manufacturing Stock Price Trend估值方法与风险声明 / Valuation Method and Risk Statement我们基于市盈率倍数对台积电设定目标价。We base our price target for TSMC on a PE multiple.我们认为台积电面临各种风险,包括技术快速变化、激烈竞争、高资本投资和周期性需求。台积电还有向员工支付股票期权的历史,这可能会稀释每股收益。We think TSMC faces a variety of risks, including rapidly changing technology, intense competition, high capital investment and cyclical demand. TSMC also has a history of paying stock options to its employees, which could dilute earnings.预测回报 / Forecast Returns